GBL Groupe Bruxelles Lambert - Diversified and Underperforming

Today we are going to dive deeper into GBL - Groupe Bruxelles Lambert. After looking at Sofina as a bet on alternative asset classes, I was looking forward to having a closer look at GBL as it also has quite some exposure to PE and VC.

GBL - Company description and asset distribution

Groupe Bruxelles Lambert was founded in 1972 by the banker Leon Lambert. Its origins can be found in the banking business. In 1982, Pargesa Holding SA took a majority, today holding around 31% of shares and 45% of voting rights. Pargesa is owned partially by the Frere family and partially by the Canadian conglomerate Power Corporation of Canada - another listed investment company. Similar to Sofina and Exor NV, GBL holds stakes in various listed and non-listed companies. However, it is much more diversified than Exor (which does not necessarily need to be a good thing).

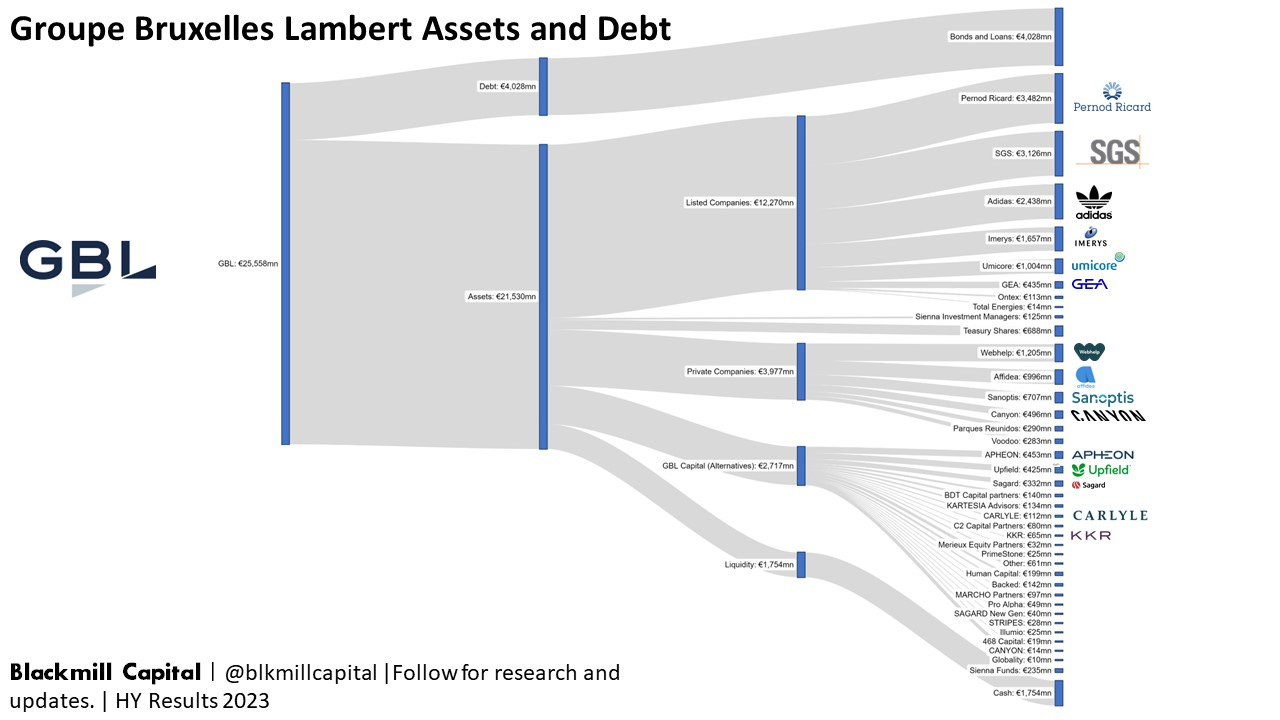

Through its alternative assets arm GBL Capital it is also invested in many growth, buyout, venture capital, and private equity funds run by well-known managers. I liked that already about Sofina as it gives me exposure to a different asset class. As of 30th June 2023 64% of its assets are listed, 21% are private companies, and 14% are attributable to GBL Capital.

In the graphic, you can see all assets and debt of GBL split up into listed, non-listed, and investments made through GBL Capital. The listed investments are concentrated with Pernod Ricard (16% of total assets), SGS (15%), Adidas (11%), Umicore (5%) and Imerys (8%). Most of these companies have been owned by the company for many years. They tend to stick to their investments. Within the non-listed companies, Webhelp and Affidea are the largest investments with 6% and 5% respectively. Sanoptics and Canyon account for 3% and 2%, while Parques Reunidos and Vodoo for 1% each.

The assets managed by GBL Capital are more diversified. They are split up into direct investments as well as growth, venture capital, and private equity funds / co-investments managed by various general partners. Direct investments include e.g. Upfield, the company that owns plant-based nutrition brands such as Rama, Becel, and ProActiv, or Globality, an AI start-up from Silicon Valley.

Relationships with various well-known general partners exist and GBL has been an investor in various funds for many years. Fund managers include global alternative asset darlings such as Sagard, KKR, Carlyle, or BDT Capital Partners. Within the GBL Capital section, no investment accounts for more than 1-2% of total assets.

The investments tend to be in companies with a leading position within their industry. This specifically applies to the largest positions in Pernod Ricard, Adidas, and SGS. Pernod and SGS also tend to be rather non-cyclical businesses.

Imerys and Umicore have a unique position at the moment with significant tailwinds. As the developed world is just beginning to grasp what will be needed in terms of materials, infrastructure, and processing capacity to complete the transformation of our energy infrastructure and automobile industry towards EVs, governments and politicians also realize how much we depend on China. Imerys is involved in various lithium mining projects in Europe1, while Umicore is a global leader in the production and recycling of special materials and components that are needed for the automotive, chemical, and construction industries. In October 2023 the company just announced it would expand its production capacity in Poland for the production of cathodes and battery materials for Volkswagen. GBL owns close to 16% of Umicore and is the largest shareholder.

If we look at the other privately owned companies there are also global leaders to be found. Affidea, for example, owns over 300 medical centers in Europe operating diagnostic imaging (MRI, CT Scanners), and cancer care machines. It also provides primary care services and laboratory services. In short, services that are needed with an aging population.

After the approved merger Webhelp and Concentrix formed a power horse for various technologies that will benefit from digitalization and AI in the medium term. This includes services for sales outsourcing, customer experience design and strategies, data and analytics, or digital marketing. Since GBL’s entry in 2019, there has been an expansion from 35 to over 60 countries worldwide, while the employee numbers more than doubled. The results of this are likely to be seen over the next few years.

Performance and Financials

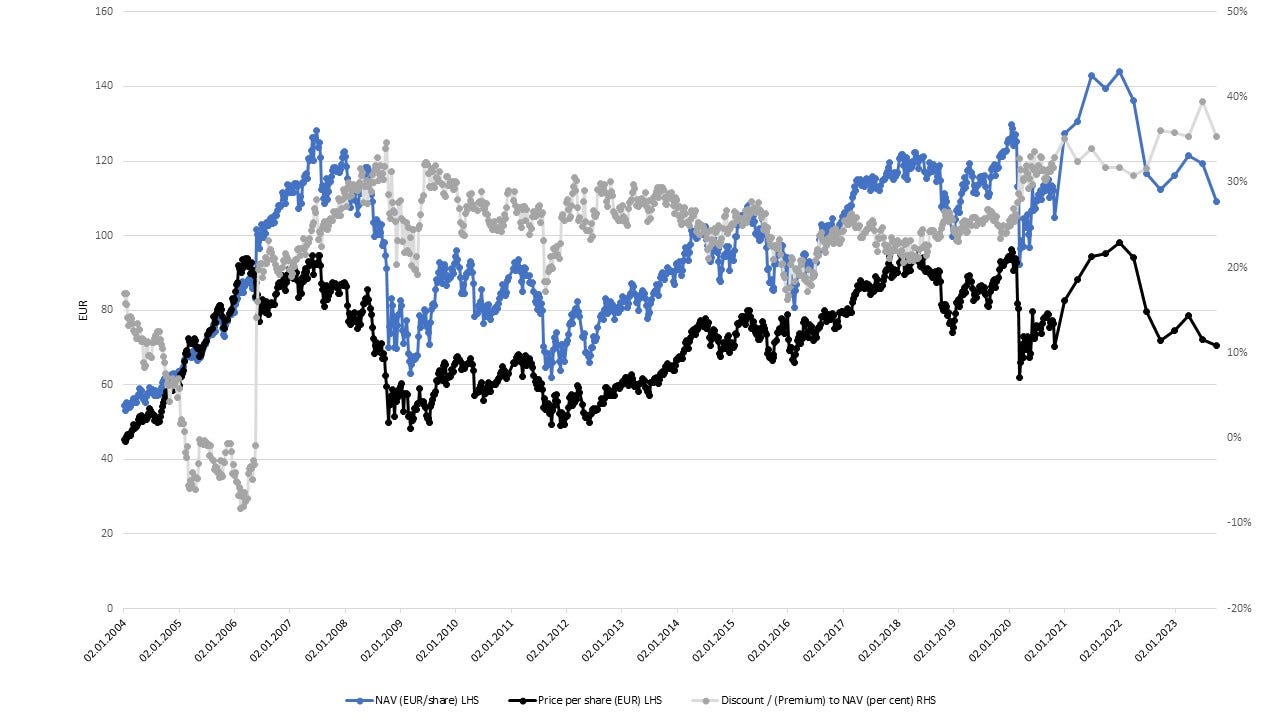

As much as I like the diversification of the portfolio the performance of GBL shares is mediocre. Since 2004 its NAV per share has gone from 54 to 110 EUR, which is a CAGR of 3%. This is also reflected in the share price growth from 45 to 70 EUR roughly. The discount to NAV has usually been between 20% and 30% with a recent trend towards 40%. I will get further into the reasons below and why there is a chance for improvement.

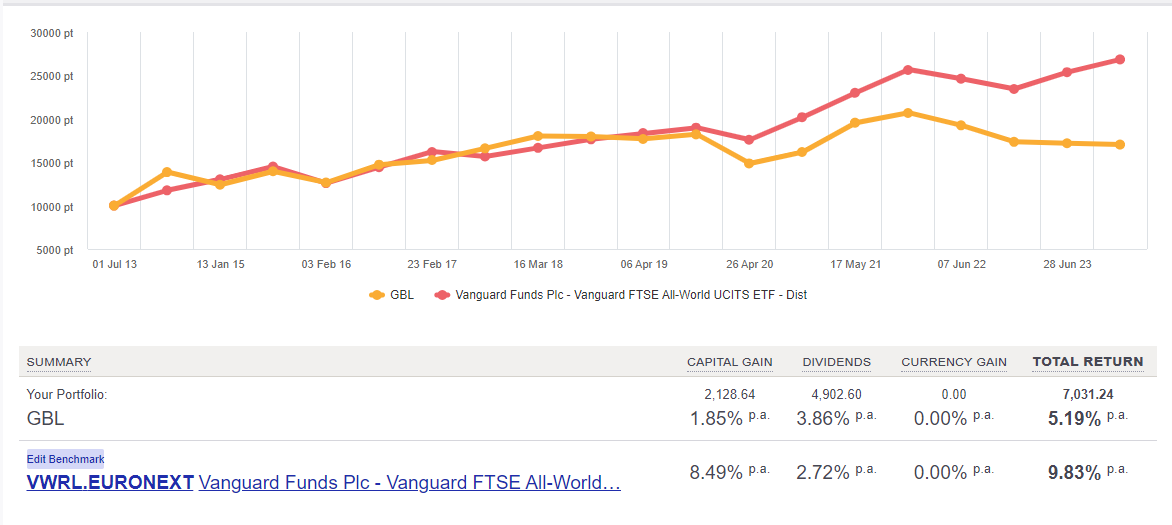

Also when we look at the last years GBL underperformed the benchmark significantly. Without dividends, there was a capital gain of only 1,85% annualized. If we look at the chart of NAV it’s clear where that comes from - there can be no shareholder value if NAV per share increases at a CAGR of 3%.

If you look at the graphic above you can see that cash earnings over the past 11 years have been pretty much flat for GBL. These consist mostly of dividends that the portfolio companies paid. In the future, there will also be realizations from the portfolio, payouts from funds, and so on. I believe it’s quite safe to assume that at least 300-400 million EUR could be used each year for buybacks instead of a dividend payment if capital is allocated efficiently which would amount to 3-4% each year of the current market cap. In general, I prefer buybacks over dividends due to tax efficiency. Of the roughly 4 billion EUR in debt, 2,5 billion EUR mature after 2028 and with the current cash position of 1,4 billion EUR, I do not see any problems arising from the financial side for GBL. The question is only how capital is invested in the future and whether there is hope that the discount to NAV will be smaller.

Recent Developments and Future Outlook

What I like about the company is its diversification of assets and the company portfolio. As investors, diversification is the only free lunch we get in finance. These tend to be less cyclical businesses, leaders in their respective industries, and a recent shift towards more private investments than listed. What I do not like is the share price performance. Looking through analyst presentations, annual reports, and also capital market day documents I found that there is a slight chance that the management of GBL has understood how to improve shareholder value. While I have so far no objections to the portfolio companies of GBL I think there is (or was) a problem with capital allocation.

The company has realized this and committed to buybacks of roughly 600m EUR in FY2022, while their projections go for 810m EUR buybacks for FY20232. Corporations tend to have poor timings on buybacks, but given the current discount to NAV, this does seem like one of the better times.

In November the company also sold its stake in GEA delivering on the promise to reduce its allocations in listed assets and streamline the portfolio3.

GBL aims to decrease the number of listed portfolio holdings while at the same time, it seeks to increase investments in private assets4. It also sold some of its Pernod Ricard shares seizing the opportunity while the share price was still high. This was before Pernod Ricard got sold off in line with other “unhealthy” companies like Coca-Cola, Pepsi, General Mills, Diageo, or Brown Forman. Likely all out of fear that the new GLP-1 / Ozempic medication would reduce overall consumption of these products in the future. I may do a separate post on GLP-1 soon

The dividends from GBL’s largest investments should be fairly safe even in case of an economic downturn. This will give GBL further opportunity to allocate capital in the future. Given the improvements in the capital allocation strategy (probably) in the recent past, it seems a bit odd that the discount to NAV is at an all-time high.

I have no opinion here in the short term. I do not make predictions on companies. At the moment I am just looking at these holding companies to find possibilities to diversify my portfolio into different asset classes as far as possible. Citing from a very famous and wise movie scene below:

I do not make these predictions. I am looking forward to the FY2023 report of the company and will continue to monitor recent developments. If I had to choose I would prefer Sofina over GBL at the moment.

This is no financial advice, please read the disclaimer, too.

https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/metals/121123-infographic-europe-lithium-projects-mining-push-regionalize-battery-supply-reduce-import-dependence

https://www.gbl.com/en/media/3979/20230731%20GBL%20-%20HY23%20results%20presentation.pdf

https://uk.marketscreener.com/quote/stock/GEA-GROUP-AG-436397/news/Gea-loses-major-Belgian-investor-GBL-share-price-drops-significantly-45405140/

https://www.gbl.com/system/files/public-files/GBL%20CMD%20-%20ONLINE%20Deck%20-%20DARK%20-%20Conclusion.pdf

Disclaimer

The information found in this document or in general in any article, document or post published by Blackmill Capital or on https://blackmillcapital.substack.com is neither investment advice, nor does it express any viewpoint on the future prices of any security or asset class. The opinions and information should explicitly NOT be taken as guidance to make any investment decisions. Investors should conduct their own research, rather than relying on the content herein. Neither the publisher nor affiliates assume liability for any direct or consequential losses arising directly or indirectly from the use of the information provided in this content. Blackmill Capital is a publisher of financial information and does not function as an investment advisor. Personalized or tailored investment advice is not offered. The information presented on this website does not cater to individual recipient needs. Please do your own research and seek your own advice from a qualified financial advisor. Blackmill Capital does not validate the adequacy, accuracy, or completeness of information provided. Neither the publisher nor any associated parties make any warranties, explicit or implied, regarding the information's accuracy or the use of the site.

Investing in securities carries substantial risk, and investors should be prepared for potential loss. Each individual should independently assess whether to invest based on their own analysis.