EXOR N.V. - Estimating a more conservative NAV

The first company I am going to analyze in my series on listed investment companies is EXOR NV.

Origins

The origins of this company can be traced back to the 19th Century. Giovanni Agnelli founded FIAT in 1899 in Torino, Italy. Throughout the years he acquired stakes in other companies across various industries such as food, financial services, and even newspapers. He grouped them together into a holding company called IFI in 1927 which later emerged into Exor.

Today, shareholdings in automobile companies still make up a large part of the company's assets although the focus for the future has recently shifted towards healthcare and luxury. The company is still majority-owned by the Agnelli family.

Exor’s Strategy and Business

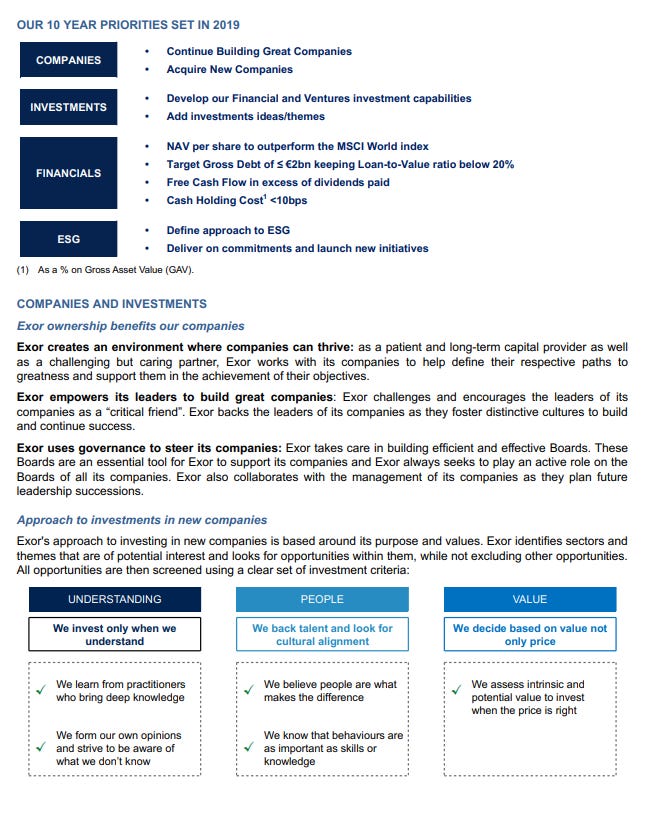

Exor’s business is easy to explain. The company is a holding company and capital allocator. Exor invests in companies with a long-term perspective. The company likes to buy significant stakes in companies. It then proceeds to appoint board members to the company and makes sure that the interests of directors and shareholders are aligned. Below is an overview of Exor’s investment goals and the company’s overall philosophy:

Exor acts more like a partner for the portfolio companies, focusing on intense discussions on strategy and strengthening the role of independent directors.

Exor does not describe this in detail, but the strategy behind this is likely that homogenous boards do not produce the best results. If a company is run like a ship and the captain needs to make all decisions independently without consultation with his officers and other experts, then it is more likely to fail at some point.

Exor gets funds in the form of dividends from their holdings, but also sometimes divests stakes in companies and reinvests those profits. In 2022 for example the company completed the sale of PartnerRe, a global reinsurance company, to Covea for 9,3 billion USD1. It acquired PartnerRe for 6,9 billion USD in 20152.

Portfolio Structure

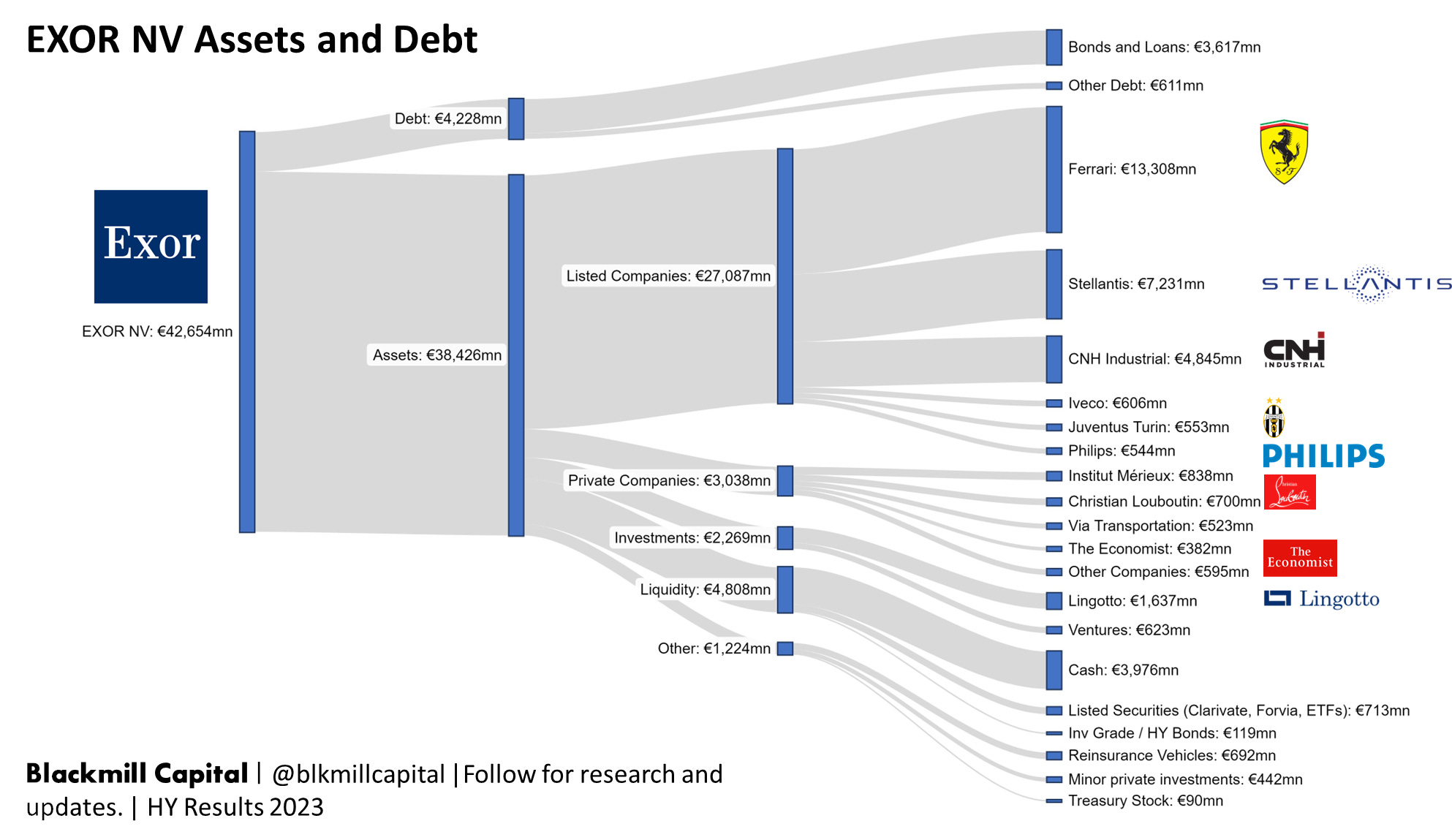

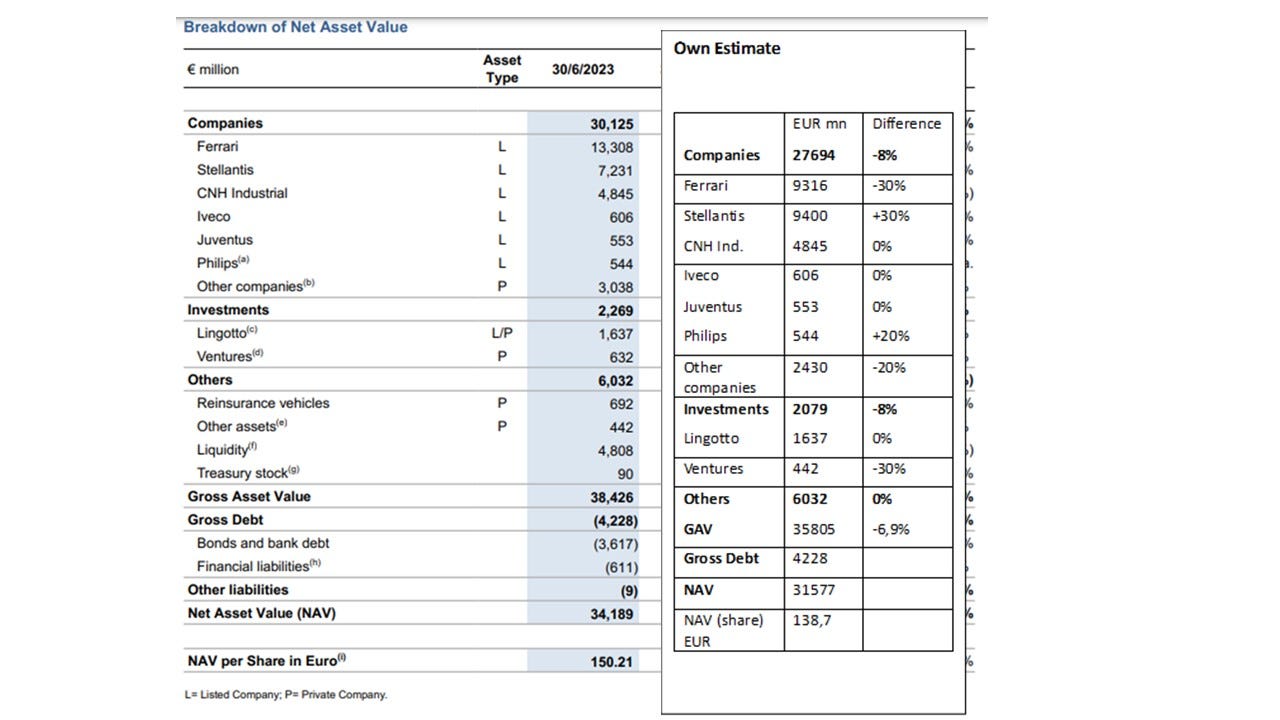

I have visualized the current portfolio, assets, and debt of Exor NV. The graphic is based on data from the first half of 2023.

35%, 19%, and 13% of Gross Asset Value (GAV) are concentrated in Ferrari, Stellantis, and CNH Industrial. Other investments include stakes in private companies like Louboutin or The Economist. Exor also has committed 1,6 billion EUR to its own investment management company Lingotto. Lingotto will manage Exor’s and Covea’s assets but will also be open to third-party assets in the future investing in private equity, long/short, and long-only strategies. The management team at Lingotto overall has an appealing profile, recently adding James Anderson from Baillie Gifford for example.

Liquidity was 13% of GAV as of the HY 2023 report with a cash position of close to 4 billion EUR. I like this very much – in a market downturn, this gives a company like Exor an edge over other players as they have cash that they can put to work and take the opportunities provided by the market.

The company currently has a market cap of 22 billion EUR. Taking just the value of the listed companies at 27 billion EUR, adding the cash of 4 billion and subtracting the debt of 3,6 billion EUR shows that basically, the company is trading at less than the value of its listed stock holdings. All non-listed assets are not being accounted for by the market.

Debt is not a concern for Exor as they could easily pay down debt immediately using cash. Bonds and loans are close to 3,6 billion EUR compared to total assets of more than 38 billion.

Portfolio Companies

I will not get into too much detail on the portfolio companies as this would require a completely separate valuation. I like to keep it simple and I find DCFs quite useless, as it is impossible to exactly forecast a company’s future cash flows. I will comment on a few thoughts regarding the companies below.

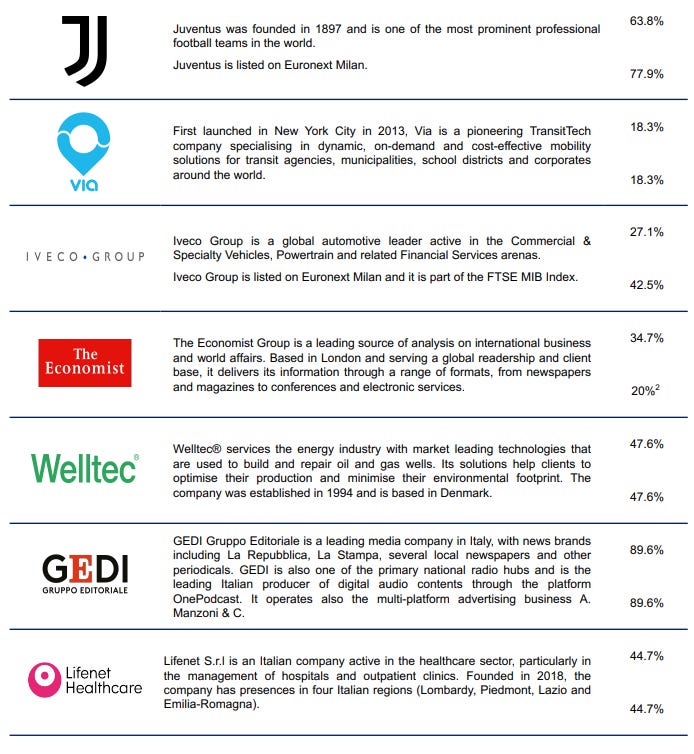

First of all, this is an overview of Exor’s portfolio companies taken from a company presentation:

Ferrari

Ferrari is one of the leading brands of luxury sports cars. Over the past years, the company has shown consistent top-line growth. Revenues increased from 2800 mnEUR in 2015 to 5000 mnEUR in 2022. I believe the company is positioned to grow further as its clients are less sensitive to economic challenges. The issue I have with Ferrari is its current valuation. It is expensive by any metric whether that is EV / EBITDA at 30,38x, forward PE of 40, or P/S at 10,7x3. It is still a car company, but it is trading at aggressive growth multiples which will likely not occur in the way the market is pricing it at the moment. Therefore later on in my valuation, I would like to take a conservative approach and reduce the value of Exor’s stake in this company by 30%.

Stellantis

Contrary to Ferrari trading at very low multiples. I like the CEO Carlos Tavares. He turned around Peugeot from a business that was losing billions in 2012 to 3 bn EUR of profits in 2018.

Peugeot is a part of Stellantis now. While I agree that the brands of the company overall are not very sexy such as Alfa Romeo, Chrysler, Citroen, Fiat, Jeep, Opel, and Peugeot, I think electrification is a huge opportunity for Stellantis. It will require huge amounts of CAPEX that is true. Stellantis had a net income of more than 16 billion EUR last year and this year is on track to perform even better. Taking into account the debt it currently has an Enterprise Value of 42 billion EUR which leaves us with an EV/EBITDA of 1,34x (remember Ferraris at 30,38x?). Volkswagen for example currently trades at an EV/EBITDA of 3,68x, Ford at 6,2x. The discount for Stellantis seems a bit high here. At Peugeot Carlos Tavares was able to bootstrap the whole production down to 2 platforms only reducing costs significantly. With electrification in progress and a changing need for mobility across new generations (i.e. shared economy), I believe that Stellantis is in a position to create affordable vehicles for the masses. Electrification will be a huge game changer for manufacturers and my thesis is that it will be much more difficult for manufacturers situated in the upper middle to continue to charge premium prices (think of VW or Ford). Cost-effective manufacturers will have an edge over their competition. I like Exor’s stake in Stellantis here much better than if it had a stake in Volkswagen or Ford.

CNH Industrial

The overall industry has favorable tailwinds. While we are now experiencing a slowdown in the construction industry as high interest rates show their impact, the industry will keep growing over the long-term. Infrastructure in the US and in Europe will require significant investments over the next decades. Electrification of the economy through EVs and hydrogen will require adjustments in infrastructure. The agricultural industry also has a positive outlook. Automation will lead to a higher demand for new vehicles and equipment. Furthermore, small farmers continue to disappear and large farming corporations continue to gain market share which makes them overall stronger and increases demand for vehicles. Last but not least at some point we will have solutions for the agricultural industry with EVs or with vehicles based on hydrogen – something that will also have an impact on CNH as a cycle of equipment renewals will start.

Philips

Philips is focused on three different segments: Connected care (digital solutions), Diagnosis and Treatment, and Personal Health (chronic disease solutions). It will benefit from long-term growth with an aging population across the world. Share price has seen steep declines during the past 2 years and Exor took that opportunity. The reason was a recall in ventilators in the United States because of foam pieces and chemicals that could be breathed in by patients due to a polyester-based polyurethane (PE-PUR) foam used in these devices. Additionally, the FDA has recently received a surge in reports of signs of overheating including fire, smoke, and burns while using the device. As if this was not enough for now the company has seen slowing demand, especially from China. I think this will likely not get any better in 2024, it will probably get worse before it gets better. We are also looking at the potential for a billion-dollar lawsuit here. I do not think Philips will end up like Bayer after its catastrophic Monsanto takeover, but I think that until these issues do not get resolved the share price will likely stay at current levels. In the long-term, I believe this company will be just fine.

Institut Merieux

The company is family-lead and I like its business. As a leader in diagnostics, devices, and laboratory equipment, it delivers the picks and shovels to the healthcare industry also taking advantage of long-term trends and an aging population.

Back-of-the-envelope valuation

Accounting for some of my assumptions like the overvaluation of the stake in Ferrari I would like to get into a back-of-the-envelope valuation of Exor estimating a more realistic NAV and a more realistic discount.

On the left side, you can see Exor’s breakdown of NAV taken from the half-year report 2023. On the right-hand side, I have added my estimate. I decreased the value of the Ferrari stake by 30%. Stellantis and Philips have upside potential therefore I increased their values. I have also decreased the value of “Other companies” such as Christian Louboutin or The Economist just to be conservative. The value of “Ventures” - mainly investments in startups and growth (VC) - was also decreased by a whopping 30% to be more conservative. I do not want to say that the valuations provided by Exor (or rather by an independent third party) are not true, I just want to use more conservative figures for my calculation.

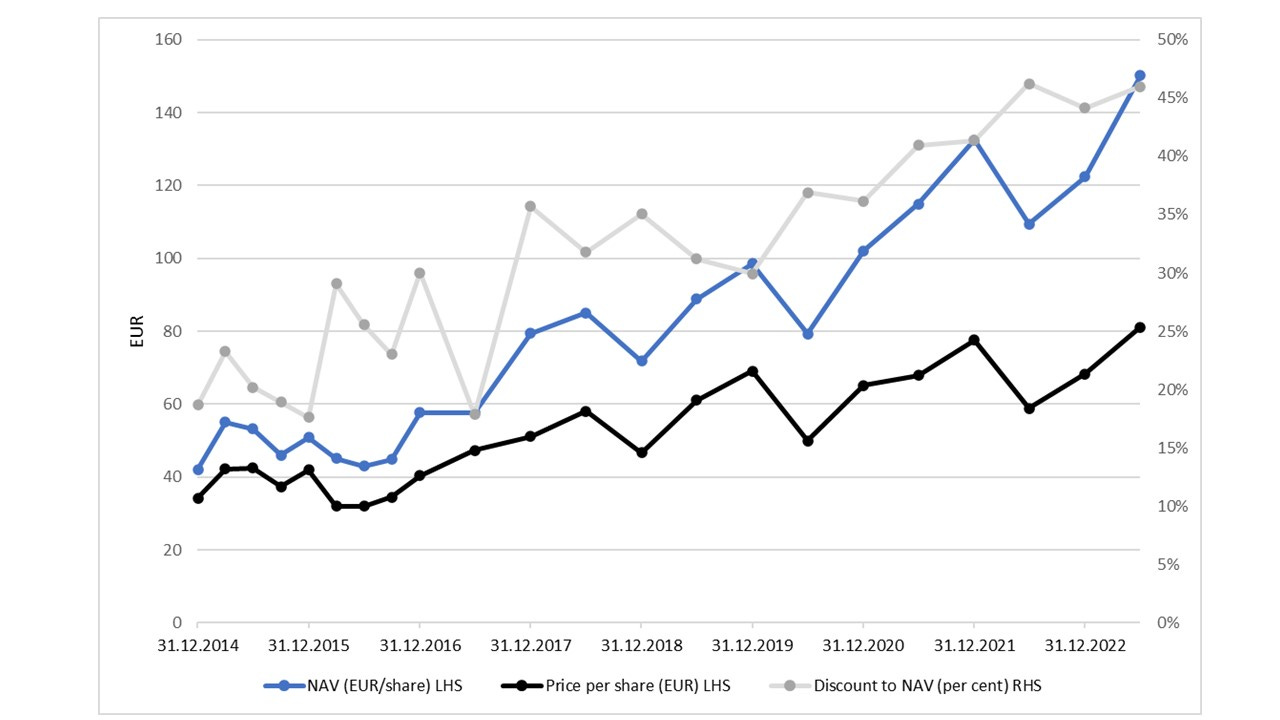

Taking all adjustments into account I arrived at a GAV of 35805 mnEUR compared to 38426 mnEUR as reported. This reduces the NAV per share to 138,70 EUR vs. 150,21 EUR as reported. Today on the 13th of December 2023 the stock is trading at 93,74 EUR. My conservative discount to NAV here is more like 32% than the reported 48%. Is that still too high? Let’s see how the stock has traded historically.

This graph shows the NAV per share (as reported by the company) and the price per share on the left-hand scale. On the right-hand scale is the discount to NAV (so the difference between share price and NAV). It is visible that while share price and NAV have continuously increased - so has the discount. In 2015 the discount was at less than 20% (right-hand scale) reaching its low and has since then continuously gone up to 45%.

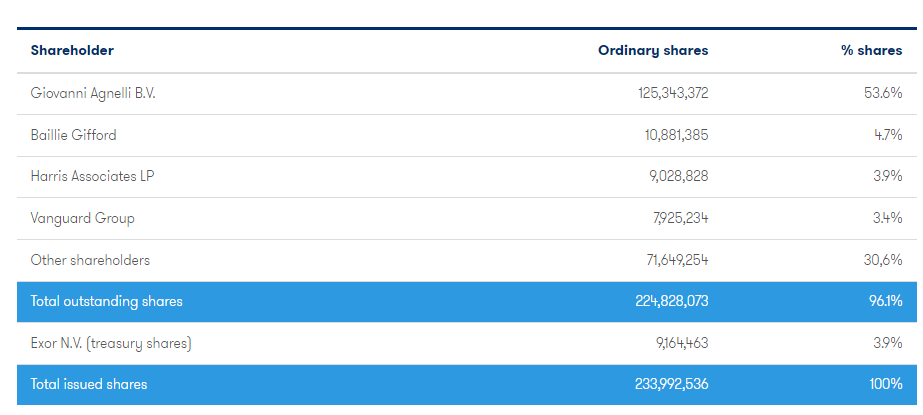

I think it is fair to say that a more reasonable discount for this holding company should probably be in the range of 20%. I fully agree that there is a possibility that the reported values of the private investments are overstated, therefore I have accounted for it. The concentration in the cyclical auto industry is probably also not the most appealing from an investor perspective as we are likely to see a slowing economy across the world within the next 12 months. I also agree with the market that because the company is majority-owned and controlled by the Agnelli family (53,6%) there needs to be a discount. With my adjusted NAV of 138,70 EUR anything below 100 EUR per share looks like there is a margin of safety in investing and room for error. I am positive about the long-term ability of this company to continue its great performance as it has in the past (see graph below). One billion EUR has been committed to share buybacks recently which will also increase the NAV/share plus I love companies doing buybacks instead of paying a dividend as this is the most tax-friendly solution to the shareholder. I am excited to see where this company will go from here over the next 2-3 years.

Exor NV has increased its stake in Philips since the HY 2023 report. As soon as there are more details on this and Exor publishes new data I will update my analysis immediately.

Please read the disclaimer. This is explicitly no financial advice. Do your own research before investing.

https://www.exor.com/press-releases/2022-07-12/exor-completes-sale-partnerre-covea-total-cash-consideration-93-billion

https://www.artemis.bm/news/exor-acquires-partnerre-for-6-9-billion/

https://finance.yahoo.com/quote/RACE/key-statistics/

Disclaimer

The information found in this document or in general in any article, document or post published by Blackmill Capital or on https://blackmillcapital.substack.com is neither investment advice, nor does it express any viewpoint on the future prices of any security or asset class. The opinions and information should explicitly NOT be taken as guidance to make any investment decisions. Investors should conduct their own research, rather than relying on the content herein. Neither the publisher nor affiliates assume liability for any direct or consequential losses arising directly or indirectly from the use of the information provided in this content. Blackmill Capital is a publisher of financial information and does not function as an investment advisor. Personalized or tailored investment advice is not offered. The information presented on this website does not cater to individual recipient needs. Please do your own research and seek your own advice from a qualified financial advisor. Blackmill Capital does not validate the adequacy, accuracy, or completeness of information provided. Neither the publisher nor any associated parties make any warranties, explicit or implied, regarding the information's accuracy or the use of the site.

Investing in securities carries substantial risk, and investors should be prepared for potential loss. Each individual should independently assess whether to invest based on their own analysis.